China Car Market Shifts from Price Wars to Rivalry in New Models, Overseas Expansion

Extreme competition among automakers in China has shaved profits and long drawn criticism from market regulators and players alike. A year ago, the China Association of Automobile Manufacturers advocated an end to industry price wars. Twelve months on, what's changed?

The short answer is that direct price cutting and buyer discounts have ended, but the fierce competition continues. Still, the China Passenger Car Association said the market has turned more rational this year.

"In 2026, 77 models have had price reductions, four fewer than last year," said Cui Dongshu, secretary-general of the association. "Models with price cuts are gasoline-powered vehicles due to the current high oil price started by the Iran war, while price reductions for pure electric models have decreased."

In fact, more than 15 makers of new-energy vehicle have announced price rises or tightened purchase conditions due to higher costs of production materials like memory chips and lithium carbonate used in batteries. That comes on top of the government's halved subsidy on purchases of green cars, making the cars more expensive.

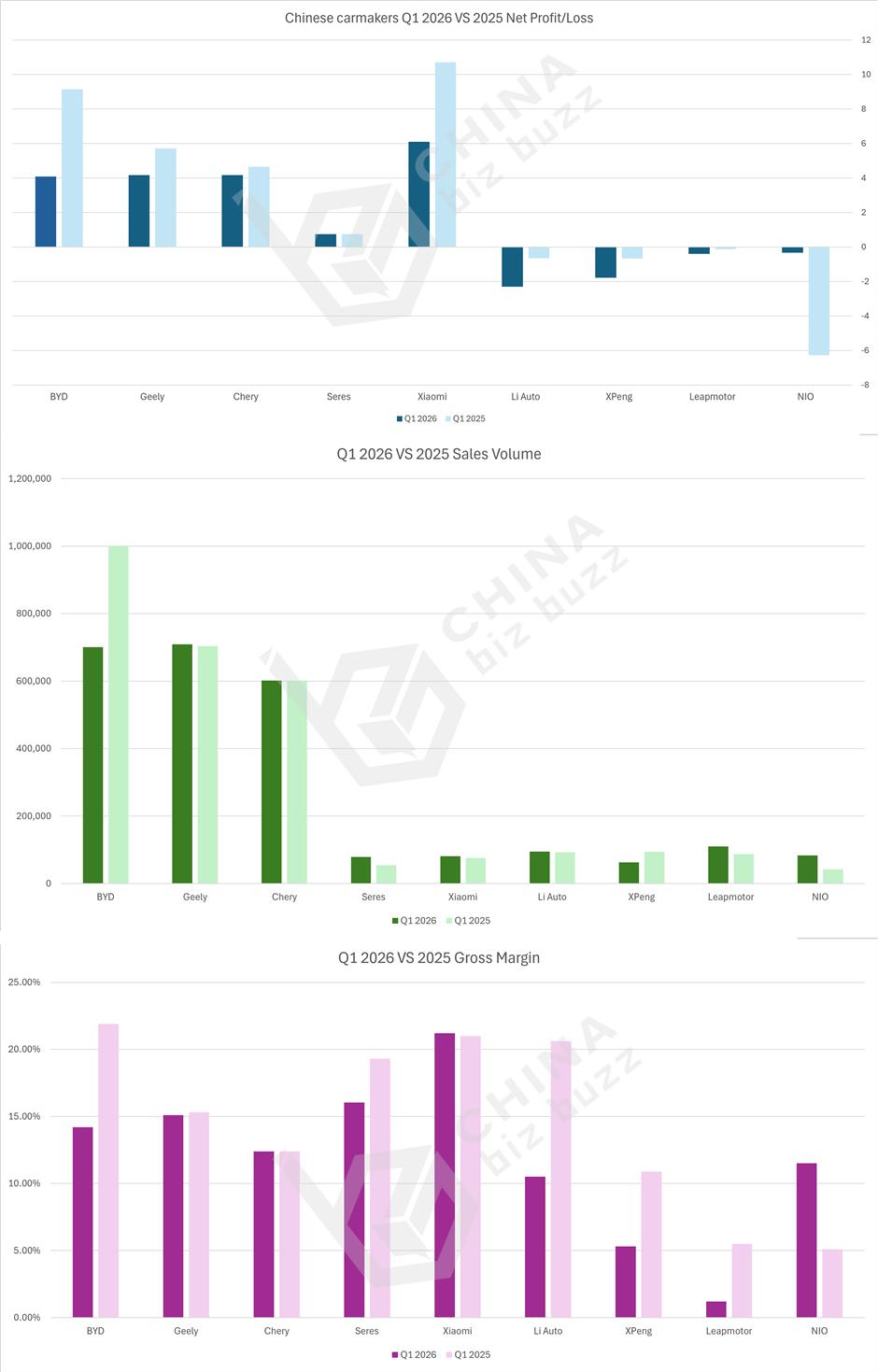

For example, BYD, the biggest manufacturer of electric vehicles, has increased the price of its God's Eye B assisted driving lidar option package for select models by 2,100 yuan (US$294), while some Nio showrooms have eliminated the 10,000 yuan terminal discount, increasing consumer costs.

Competition among automakers, however, has escalated, across technology, new car releases and overseas expansion, sometimes to a brutal stage.

In technology, equipping cars with luxurious features at standard prices has become a strategy adopted by many automakers.

The Leapmotor A10, launched in March, is one example. The model has a starting price of 65,800 yuan, rising to 86,800 yuan for a full range of premium features. The A10 offers lidar and driving capabilities usually found in cars priced at 200,000 yuan to 300,000 yuan, with a driving range of 403-505 kilometers.

The result has been volume sales without profits. In the first quarter of this year, Leapmotor delivered over 110,000 units, becoming the first startup to surpass 100,000 units in a quarter. Revenue reached 10.8 billion yuan. However, gross profit margin in the period was only 9.4 percent, lower than the 15 percent of both the first and fourth quarters of 2025.

Leapmotor still maintains high research and development spending. In 2025, that amounted to 4.3 billion yuan, an increase of 48 percent from a year earlier. In the first quarter of 2026, expenditure rose 30 percent to 1.04 billion yuan. As a consequence, the company recorded a net loss of 390 million yuan in the first quarter.

Leapmotor considers this part of its overall strategy.

"We use the A10 to gather users and to later convert them with D19, D99 and other more prestige models," said Li Tengfei, vice president of Leapmotor, during an earnings call with analysts.

Will this strategy pay off? It should be noted that the configuration of the A10 is competitive in its price range, but in the 200,000 yuan-to-300,000 yuan market, competition increases. The D19 and D99 are facing off against Huawei's Aito M7 and M9, and against the Nio ES8, to name but a few. In May, Leapmotor ranked fourth in six-seat SUV sales.

Another manifestation of competition in the market is the release of new cars. Thanks to modular platforms and chassis derivation technologies, the new car development cycle of Chinese automakers has been compressed to 18-24 months, whereas the development cycle for carbon fuel vehicles is three to five years.

According to the passenger car association, Chinese automaker released 71 new and replacement models in the first five months of this year. Adding in models with modifications and advanced features brings the number to over 500, an average of three to four new cars per day.

At the Beijing Auto Show in April, global premieres rose to 181 from 117 a year earlier and concept cars increased to 71 from 41.

"The density of new product releases in the auto industry has increased," Qin Lihong, co-founder of Nio, said at the Beijing Auto Show. "This is not a strategy adjustment by enterprises based on market heat, but the realization of layouts created by the industry years ago. Individual carmakers cannot advance independently of the industry pace."

Now new product launches serve as a tool for automakers to maintain market share. Slowing down the pace of introductions results in lost online traffic, user attrition and marginalization.

The fast pace has also affected joint venture brands. For instance, in 2015, the last golden age of gasoline-powered vehicles, FAW-Volkswagen released six new cars in China. This year, it has debuted 13 new cars, half of which are new energy vehicles.

This is all reminiscent of China's home appliance market 30 years ago and the smartphone market 10 years ago.

In the 1980s and 90s, the color television and refrigerator markets in China was dominated by Japanese brands such as Panasonic, Sony and Toshiba. Then Chinese home appliance brands like Changhong, Konka and Haier emerged. In the mid-90s, Changhong initiated a price war, reducing the prices of color televisions by 30 percent.

The resulting rounds of industry price-cutting pushed foreign brands out of the mainland mass market and eliminated hundreds of smaller domestic appliance factories. The industry then consolidated into an oligopoly of Midea, Haier and Gree, all expanding globally.

The same pattern hit the mobile phone industry. Over a decade ago, after the Android system became open-source, hundreds of mobile phone brands mushroomed in the China market. Manufacturers competed on scores, camera pixels and screen refresh rates, releasing dozens of models a year. Following a consolidation between 2015 and 2018, brands such as LeEco and Gionee went bankrupt. The market in China today retains only Huawei, Xiaomi, Oppo, Vivo and Apple.

This sort of industry evolution is now occurring in automobiles. Since 2020, over 20 new energy vehicle makers have declared bankruptcy, entered liquidation or begun restructuring. The Chinese market today has 40-50 companies turning out new energy vehicles, including startups, established marques and gasoline-powered models shifting to electric and hybrid models, such as IM Motors and GAC Aion. Industry analysts are predicting further consolidation by 2030.

"In the future, there will only be five Chinese car brands with scale and sales volume, alongside several foreign companies," He Xiaopeng, chief executive of Xpeng Motors, predicted at a forum last month.

Xpeng Motors itself is facing crisis. Total deliveries for Xpeng in the first quarter fell by a third from a year earlier to 62,682 vehicles, resulting in a net loss of 1.78 billion yuan. Why? Because it didn't deliver many new models in the period.

Meanwhile, Xpeng has maintained investment in research and development, which rose 47 percent to 2.9 billion yuan in the first quarter, eroding cash reserves. Single-quarter cash outflow exceeded 5.5 billion yuan, weakening the company's ability to withstand risks.

Competition in the domestic market is forcing automakers to increase their focus on overseas markets. BYD said it plans to sell 1.3 million vehicles overseas by the end of this year, an increase of 25 percent from 2025. Leapmotor has set a goal of 100,000 overseas sales.

But restrictions in European and American markets threaten to turn blue oceans into seas of red. That caused some Chinese carmaker to focus on markets in Southeast Asia. In Thailand, BYD, Great Wall, Changan, GAC Aion and MG established factories. As a result, overall sales of Chinese brands surpassed Japanese cars for the first time in January.

But a month later, following changes in Thailand's electric vehicle subsidy policies, the market share of Chinese brands dropped to 12 percent. Although sales of Chinese automakers grew again in March due to rising fuel prices, the setbacks of February served as a warning: mainland brands trying to expand overseas can face bottlenecks.

Passenger car association executive Cui remains upbeat.

"Even with challenges, automotive companies are refining and clarifying their global strategies," he said. "Through approaches, ranging from knock-down assembly to localized production and overseas mergers and acquisitions, these automakers will become more mature and will achieve remarkable results in their international expansion."

The road to maturity may have potholes at present, but Chinese carmakers are nothing if not resilient and inventive. And anyone who writes off their chances of global prominence probably won't have the last laugh.

Editor: Liu Qi

![[Hai Guide] The Inner Ring Road Is Getting Repaired – Here's Where You'll Feel It](https://obj.shine.cn/files/2026/06/18/e218b933-1d0c-41a9-990e-ff9215f35807_0.jpg)