Japan Carmakers Misjudged China, Now They Are Scrambling to Correct the Mistake

Honda and Sony pulled the plug on their four-year co-development of the electric vehicle Afeela 1, which had begun pre-production at a plant in the US, after Honda decided to abandon its 0 Series electric-car lineup. The Afeela was already drawing criticism for its bland styling and so-so performance. Honda said it is recalibrating its electric car strategy.

The pivot comes as Honda faces an unprecedented financial crisis, warning it may post its first annual loss in nearly 70 years. For its fiscal year ending March 31, it is projecting a loss of between 420 billion Japanese yen (US$2.8 billion) and 690 billion yen.

Honda's predicament is the poster child for a severe crunch within Japan's auto industry.

While complete annual figures from Japanese automakers, based on the nation's March fiscal year, are yet to come, a look at third-quarter reports, analysts' forecasts and 2025 sales point to a severe, industry wide slump.

Nissan is projecting a net loss of 650 billion yen, its second consecutive year in the red. Last year, the company announced the closure of seven global factories and 20,000 layoffs. Its 2025 global sales fell by 4 percent to about 3.2 million vehicles, dropping the company out of the world's top 10 automakers for the first time since 2004.

Even Toyota, the bellwether of Japanese automakers, is not immune. Although it retained its crown as the world's top-selling automaker for the sixth consecutive year with 11.32 million vehicles in 2025, its bottom line took a severe hit. For the first three quarters ending December 2025, Toyota's net profit plunged 26 percent to 3.03 trillion yen. The company has downgraded its full-year profit expectations.

The gravity of the situation is not lost on industry chieftains.

"Japanese automakers are facing a future-threatening crisis that threatens their very survival," Toyota's Global Chief Executive Koji Sato told the Japan Automobile Manufacturers Association last year. "The question is how we can identify Japan's winning strategies. To survive the current difficult environment and grow as a mobility industry, I believe it is essential for the entire auto sector to unite and enhance our international competitiveness."

Many attribute pressure in the industry to trade wars initiated by US President Donald Trump. Indeed, for second-tier Japanese brands heavily reliant on the North American market, tariff policies from the US were a profit shredder.

In the first half of the 2025 fiscal year alone, Japan's top seven automakers lost a combined 1.5 trillion yen in revenue due to US tariffs.

Take Mazda for the example. The US market accounts for roughly 30 percent of Mazda's global sales, mostly driven by direct exports from Japan. Tariff barriers caused Mazda's first-half profit to nosedive, resulting in its first net loss in five years. Subaru and Mitsubishi are facing similar grim contractions.

However, another larger and far more fatal reason for industry woes is the rise and global expansion of the Chinese auto industry.

Japanese automakers can theoretically mitigate the impact of US tariffs by expanding localized production in America and shifting supply chains. But the fierce competition from China has no easy exit.

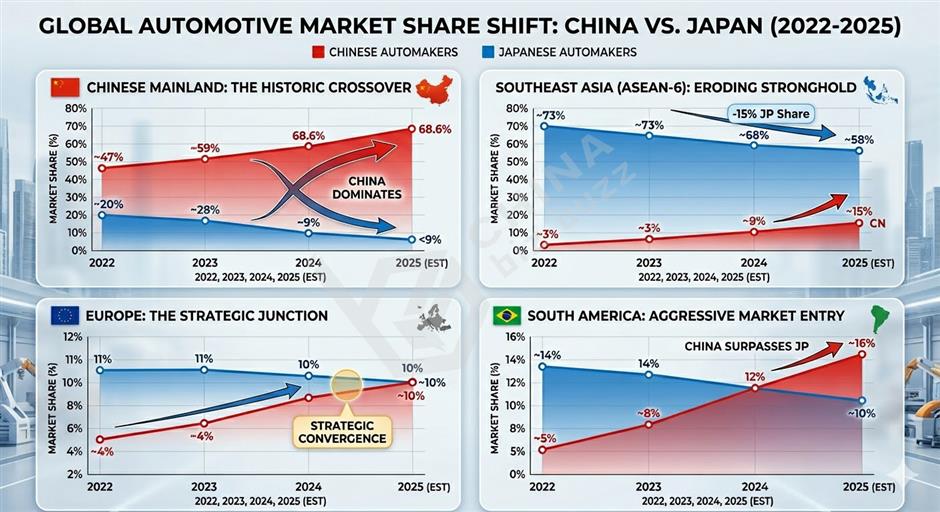

In 2025, Chinese automakers' global sales approached 27 million units, while Japanese automakers' ales slipped to roughly 25 million. It was the first time since 2000 that Japan has lost the crown for total global vehicle sales. Just three years prior, Japan led China by a comfortable margin of 8 million vehicles.

In such a short span, that massive moat was wiped out. Within China, the traditional "big three" Japanese brands – Toyota, Honda and Nissan – saw their combined 2025 sales plummet to around 3.1 million units, with their overall market share dropping below 9 percent, a stark contrast to their peak when they commanded over 30 percent of the market.

Honda is a typical example. In collaboration with the Guangdong Automobile Company, China was once its most crucial profit engine. Yet today, it is its biggest financial bleed. Faced with the competition from the likes of domestic new-energy vehicle makers like BYD, Xiaomi and Nio, who offer lower pricing and advanced smart driving features, Honda's competitiveness has sharply declined. Its 2025 sales in China fell by more than 24 percent from a year earlier, plummeting over 60 percent from its volume peak of 1.6 million vehicles in 2020 peak.

The downfall of Japanese carmakers is an inevitable result of its massive, idled internal-combustion engine capacity after two decades of global expansion and a severe miscalculation of the speed at which electric vehicles came to dominate the market.

Between 2010 and the early 2020s, top Japanese executives largely believed pure electric vehicles would take a long time to mainstream, betting their core strategy on hybrids and hydrogen models. As a result, between 2015 and 2020, they were still heavily investing in new or expanded gasoline-powered vehicle factories globally. When the electric vehicle wave hit with unexpected ferocity, these relatively new, capital-intensive facilities soon turned into massive liabilities.

Senior automobile industry critic Zhou Lei, founder of the new media outlet Auto Tittle-Tattle, said the trend was especially obvious in China, where both Japanese automakers and their Chinese joint ventures failed to grasp the policy clout of China's full-scale commitment to the new-energy vehicles.

"It was perhaps excusable that the 1-million-unit milestone for new-energy vehicle sales in 2018 didn't capture enough attention from these companies, but their failure to prioritize the sector by 2022 led to a 170 percent drop in growth – a major strategic blunder," Zhou said. "In hindsight, that period represented the most critical window for them to adjust their strategies and change their trajectory in the Chinese market."

That transition became all the more obvious last year, when overseas passenger car exports by Chinese automakers surpassed the 1 million mark for the first time.

In traditional Japanese strongholds such as Southeast Asia, Latin America and the Middle East, Chinese vehicles are eroding Japanese market share, armed with generational leaps in electrification technology and high cost-effectiveness. In 2015, Japanese brands boasted an 84 percent market share in Southeast Asia. By 2023, that fell to 68 percent and dropped further to nearly 64 percent in 2024.

But Zhou said he believes all is not lost for Japanese automakers.

"This year is undoubtedly a back-to-the-wall battle for Japanese cars, at least in the Chinese auto market," Zhou said. "We can see that they have indeed made comprehensive adjustments from a strategic level."

Last June, Toyota, for the first time, handed over the primary authority for Chinese model development to its local engineering teams on the Chinese mainland, establishing a unified new approach at its Toyota China Research and Development Center.

This marks a radical departure from the past, when Japanese headquarters defined the product and the Chinese team merely handled local adaptation. This shift is expected to significantly accelerate Toyota's response time to the specific demands of Chinese consumers.

Also last year, Nissan Motor announced that it will invest 10 billion yuan (US$1.4 billion) over the next three years to expand its China Technology Center, giving local teams the lead in vehicle development.

A Chinese proverb says: "A lean camel is bigger than a horse." Zhou said he believes it's an apt description for Japanese automakers.

"Look at Toyota. Even though it didn't closely follow the Chinese new energy vehicle market in 2020, its 2025 sales have declined by less than 10 percent from its historical peak," Zhou said. "This shows their underlying fundamentals are solid. Japanese automakers assuredly have the ability to hit bottom and bounce back."

Editor: Liu Qi